Case Study Details

About The Project

Intrinsic Valuation of Pension Fund Investments Backed by RMBS/ABS-CDOs

Client Profile

One of the largest financial institutions in the United States, with a diversified portfolio of pension fund investments across structured finance products, including RMBS, ABS-CDOs, and home equity loan-backed securities. The client serves sovereign entities and insurance companies, requiring robust credit analytics and valuation support for secondary market transactions.

Project Objective

To deliver bottom-up credit insights and intrinsic valuation for pension fund holdings backed by non-agency RMBS and ABS-CDOs, enabling informed investment decisions in the secondary market. The goal was to assess creditworthiness at the loan level and support pricing strategies for complex structured products.

Loan Performance Database- Monthly Update

Loan Scoring Model- Heuristic / Deterministic Approach

Prepayment & Default Curve- Intrinsic Valuation for Fixed Income Assets

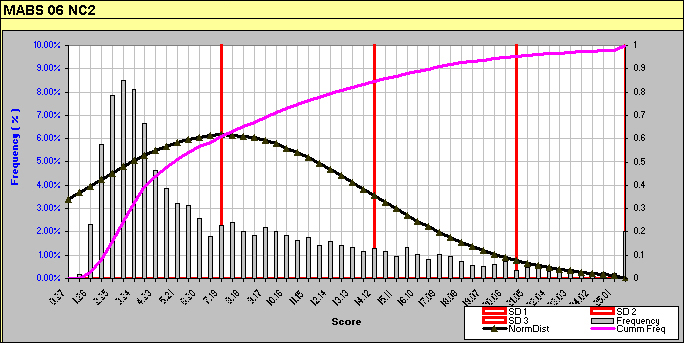

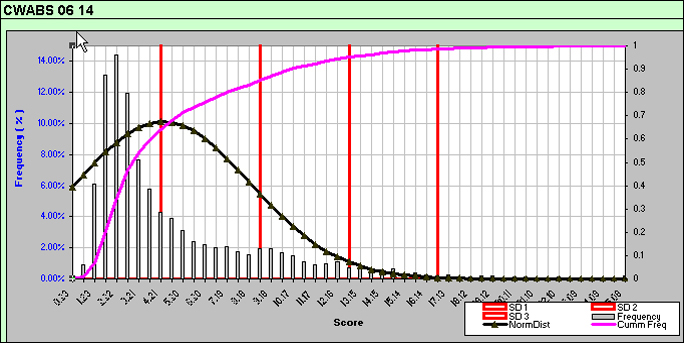

Normal, frequency and cumulative distribution of loan scores with standard deviation multiples.

Our Approach

Loan-Level Mortgage Modeling

-

Developed granular models based on individual loan performance, incorporating borrower behavior, property characteristics, and macroeconomic factors.

-

Simulated default probabilities, prepayment speeds, and loss severities under various economic scenarios.

Credit View Construction

-

Built bottom-up credit views by aggregating loan-level analytics across tranches and deal structures.

-

Integrated economic indicators such as unemployment rates, home price indices, and interest rate curves to stress-test asset performance.

Loan Score-Based Credit Model

-

Designed a proprietary Loan Score framework to rank and segment loans based on risk-adjusted metrics.

-

Enabled intrinsic valuation by mapping loan scores to expected cash flows and credit enhancement levels.

Valuation of Non-Agency Bonds

-

Applied the model to non-agency RMBS and ABS-CDO bonds traded in the secondary market.

-

Delivered pricing insights and relative value analysis for pension fund portfolios, supporting buy/sell decisions and risk management.

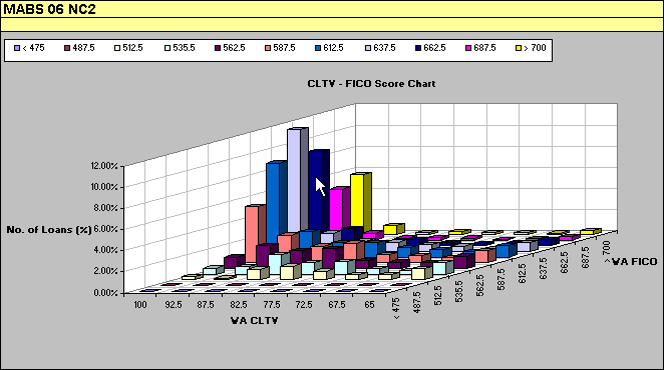

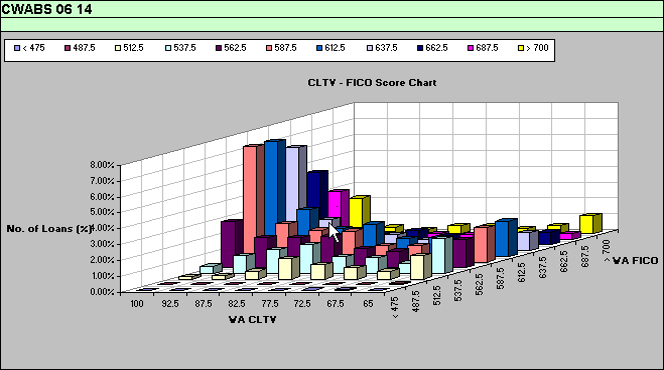

Loans Vs FICO Vs CLTV for the two deals.

Impact & Outcomes

-

Provided the client with high-resolution credit analytics that enhanced transparency and confidence in asset performance.

-

Enabled more accurate pricing and risk-adjusted return assessments for pension fund investments.

-

Strengthened the client’s ability to navigate secondary market complexities and optimize portfolio allocations.